Many people believe that preparing an insurance claim is largely a matter of estimating the value of what has been damaged.

In reality, that is often the easier part.

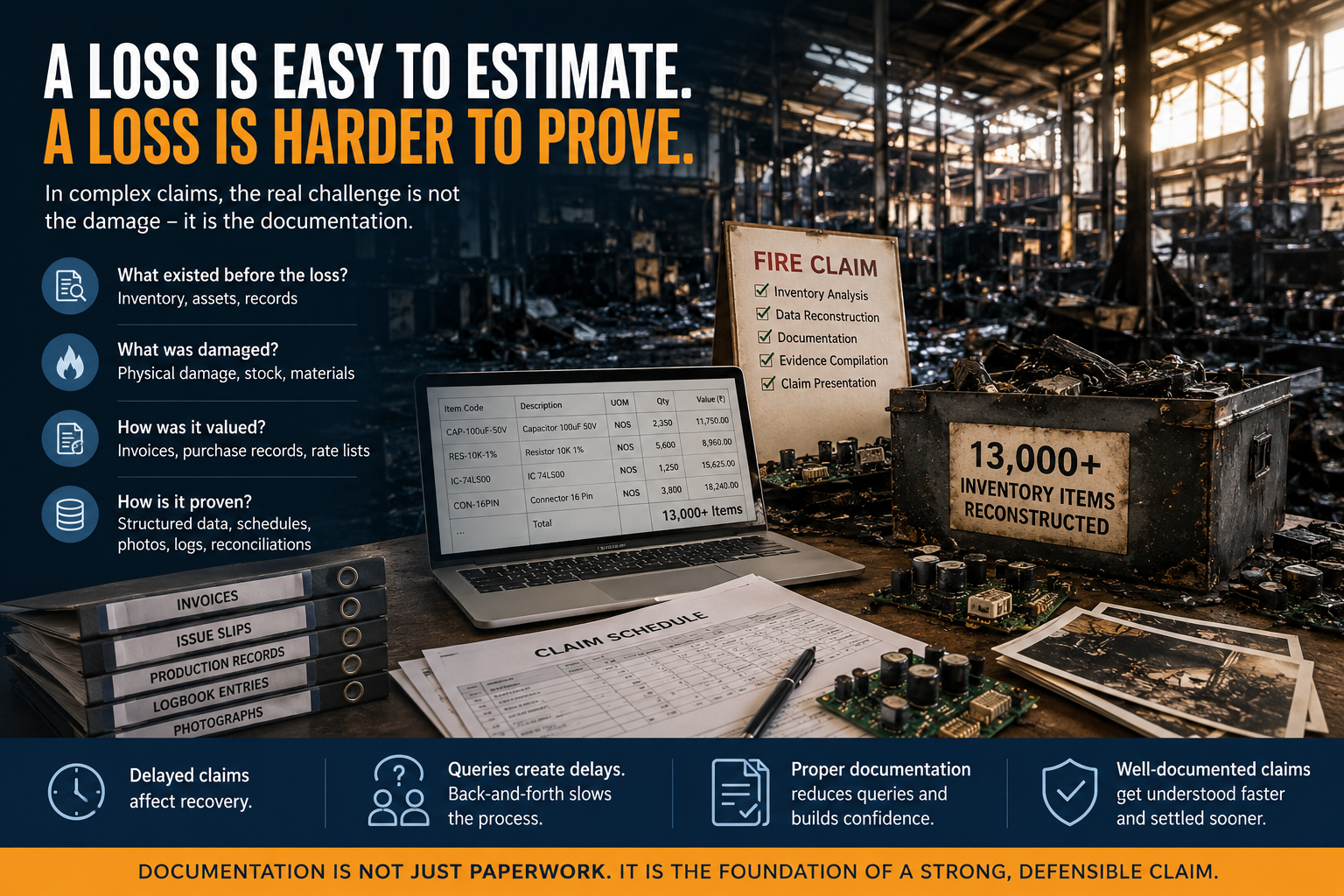

Many years ago, I was involved in a major fire claim concerning a manufacturer of electronic measuring instruments.

The company manufactured around 60 to 70 finished products. At first glance, the claim appeared manageable.

However, when we examined the inventory records, a very different picture emerged.

Behind those finished products were approximately 13,000 individual inventory items.

Capacitors.

Resistors.

Integrated circuits.

Connectors.

Specialised electronic components.

Many of these components looked similar, but tiny differences in specifications could make a significant difference to their application and value.

The fire had damaged inventory, records and supporting information.

The challenge was not simply determining what had been lost.

The challenge was proving it.

At that time, modern tools such as cloud databases, OCR systems and AI-assisted analysis did not exist.

To deal with the volume and complexity of the information, I developed a custom system using FoxBase and spent nearly fifteen days analysing, organising and reconstructing the inventory data.

The experience taught me a lesson that has remained relevant throughout my professional life:

A loss is easy to estimate. A loss is much harder to prove.

Over the years, I have often heard claimants express frustration when large claims take time to settle.

In many cases, the delay is not because the insurance company does not want to pay.

The delay occurs because the loss has not yet been fully substantiated.

Insurers, brokers and surveyors need sufficient evidence to understand:

What existed before the loss.

What was damaged.

How the quantities have been derived.

How the claimed values have been calculated.

Where supporting records are incomplete, the process naturally generates queries, clarifications and requests for additional information.

This results in back-and-forth correspondence and avoidable delays.

Unfortunately, when a major claim is delayed, the insured business may not receive funds when they are needed most. Delayed recovery can undermine one of the fundamental objectives of insurance — helping a business recover and resume operations after a loss.

This is why documentation matters.

Well-prepared claims supported by invoices, goods receipt records, issue slips, production records, stock registers, logbook entries, photographs and asset schedules are generally easier to understand, review and process.

The objective is not simply to prepare a claim.

The objective is to present a structured body of evidence that allows all parties to evaluate the loss with confidence.

The machinery may be damaged.

The inventory may be destroyed.

But if the supporting records are available and organised, a significant source of delay can often be eliminated.

Today, technology makes this task far easier than it was then.

Yet the principle remains unchanged.

A well-presented claim is not merely a statement of loss.

It is a structured body of evidence.