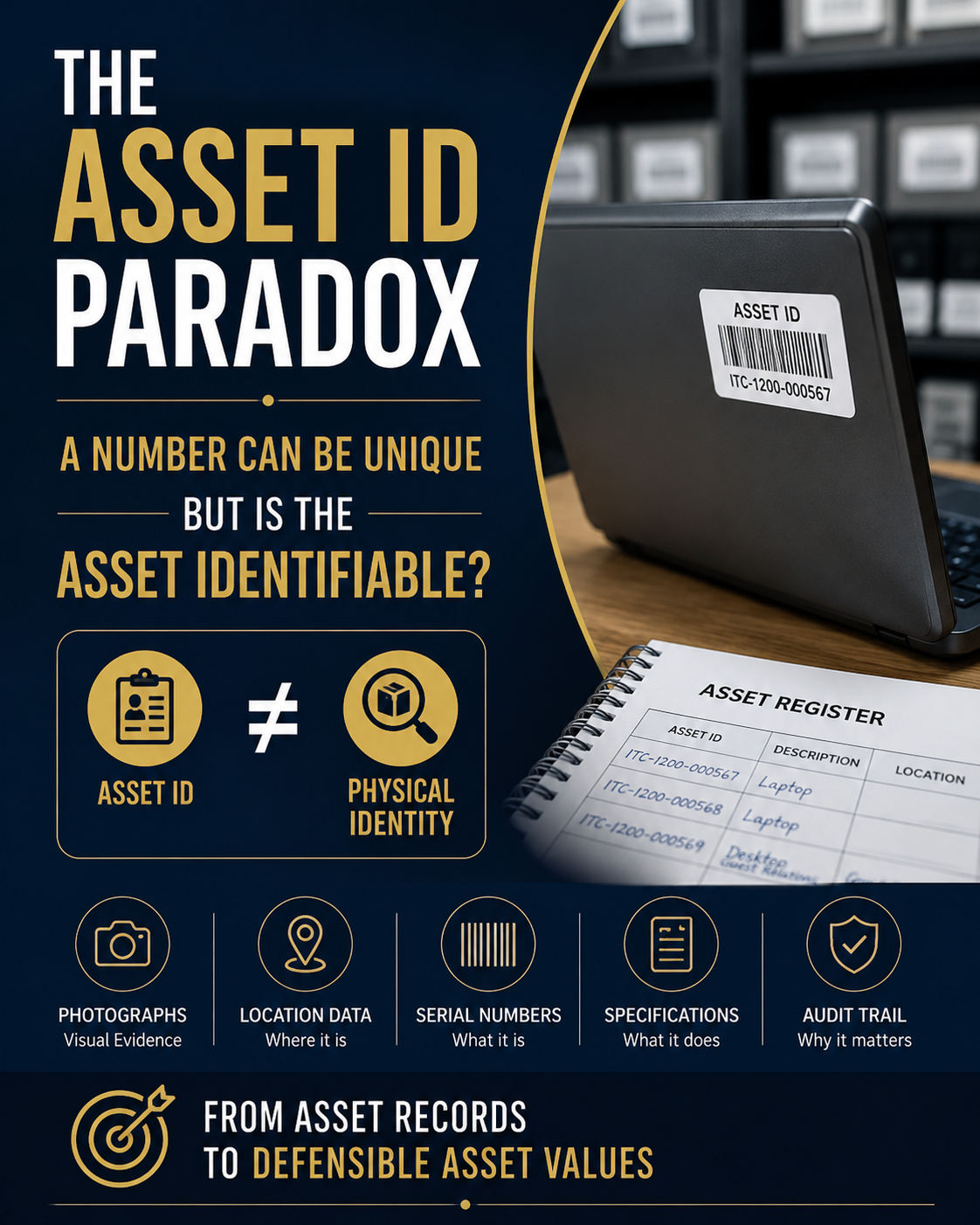

In fixed asset management, we often assume that assigning an Asset ID solves the identification problem.

.

It certainly helps.

.

But does it completely solve it?

.

Consider a simple example.

.

Suppose an organization owns 100 identical laptops purchased in the same year.

.

Each laptop may have a unique Asset ID.

.

From an accounting perspective, the assets are unique.

.

But from a physical verification perspective, can we confidently identify which laptop is which?

.

The challenge becomes even more interesting when we move beyond laptops.

.

Consider furniture, televisions, air conditioners, network switches, desktop computers, or hundreds of similar guest room assets in a hotel.

.

The Asset ID may be unique.

.

The physical appearance may not be.

.

This is where many organizations discover a gap between:

.

Asset Identity

and

Asset Identifiability

.

An Asset ID answers:

Which record is this?

.

Physical verification attempts to answer:

Which physical asset is this?

.

Those are not always the same question.

.

The larger the organization, the greater the challenge.

.

Over time, assets are relocated, upgraded, repaired, replaced, grouped, or described in generic terms.

.

The accounting record remains.

.

The physical trail becomes weaker.

.

This does not mean existing systems are wrong.

.

Far from it.

.

Asset IDs remain essential.

.

They are the foundation of asset control.

.

The question is whether additional layers of evidence can strengthen the connection between the record and the physical asset.

.

Photographs.

.

Location records.

.

Manufacturer and model information.

.

Serial numbers.

.

Specification data.

.

Together, these create a richer audit trail.

.

In the end, effective asset management is not merely about assigning a unique number.

.

It is about creating sufficient evidence so that the asset can still be understood, identified, and defended years later.

.

Especially when the information is needed most.